I Imagine, one fine morning you woke up and you needed to do some regular maintenance of your vehicle. Imagine that notification got sent to your service vendor automatically from your car along with required parts for the car. Your car has its bank account from which it can automatically order the required services and spare parts as well. Bank will notify you for transaction approval. So, you don’t need to worry about either the payment or the services.

I Imagine, one fine morning you woke up and you needed to do some regular maintenance of your vehicle. Imagine that notification got sent to your service vendor automatically from your car along with required parts for the car. Your car has its bank account from which it can automatically order the required services and spare parts as well. Bank will notify you for transaction approval. So, you don’t need to worry about either the payment or the services.

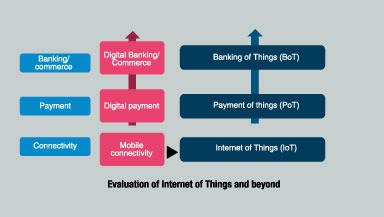

Although this is still in the innovation phase, it is not a far-fetched projection at all. In the near future we will experience astounding innovations in the financial services. This will be achieved with nothing but a connected ecosystem comprising of objects, connectivity and application/services – the Internet of things (IoT).

Imagine walking onto a car dealership and receiving an alert from your mobile banking app that automatically tells you how much financing you’ve been approved for. Even better, the auto loan application can be completed using your smartphone and contain prepopulated data stored from previous transactions. Imagine an app offering you a deal if you purchase the exact car you’re looking at. The app can send offers such as, “Save BDT 50,000 on that new “WVZ” 2017 Model, if you use “XYZ” financing.” This may seem like a “too good to be true” scenario, but with IoT and Big Data, this is something retail banking institutions could start doing today.

Just imagine the scenario where customers would be encouraged to build a product or a service like home loan or savings account, and decide the interest rate. Banks will approve the rate considering financial risk and profit analysis. Also banks can analyze the behavioral factors such as customers’ payment and expenditure pattern.

What if home appliances could signal when they are about to malfunction? What if the appliances could place orders for their replacements or schedule repair and also initiate payments, on behalf of customers? Effectively, BoT could transform any device into a point of sale terminal, placing orders and seamlessly connecting to online payment systems. Data, read by smart sensors embedded in all such objects, would be streamed continuously to a cloud based analytics platform. Banks could abstract and combine this information with other transactional data to proactively alert customers regarding the payment and transaction.

On the other hand, Banks also need to put light with priority on consumer side. They need to engage customers in discussions around sharing data for personalized services. Location based offers, personal financial management, proactive advisory are instances of solutions that depends on customers’ willingness to share personal information in exchange for convenient, contextual, customized advice and services.

A lot of excitement exists around the technology called Internet of Things or IoT. It could be better  understood if we think of it as a framework, not a technology.

understood if we think of it as a framework, not a technology.

IoT presents an incredible opening for financial services, but it also presents a serious challenges. And these are security challenges. Of course, it does not mean that we will not adopt the new technology as part of digital transformation, rather we will enhance the security features to project them.

IoT presents an incredible opening for financial services, but it also presents a serious challenges. And these are security challenges. Of course, it does not mean that we will not adopt the new technology as part of digital transformation, rather we will enhance the security features to project them.

In addition to the innumerable new applications for digital banking, IoT is also expected to generate a superfluity of data. This data is coming from a variety of new sources, at high-velocity and in increased volumes. Rising operational cost have led banks to explore technological innovation to minimize the operational cost and hence try to reduce the total cost of ownership.

Undoubtedly, innovation of a technology shouldn’t be the reason for considering it. Given the pace at which new technologies are introduced, it’s easy to get  blinded and side-tracked by the complete brilliance of the variety. Practical use cases are very important to evidence the real benefits of any. If we do the deep drive how IoT can transform banking, there are many scenarios whether IoT and Banking will benefit not just the customer but the banks as well.

blinded and side-tracked by the complete brilliance of the variety. Practical use cases are very important to evidence the real benefits of any. If we do the deep drive how IoT can transform banking, there are many scenarios whether IoT and Banking will benefit not just the customer but the banks as well.

banks must find ways to stay relevant in terms of inventing new experiences. New products, services or business models can be initiated through banking of things. New concepts can be introduced where the products are designed and led by customers. And day to day machine learning can enhance and mature the products.

IBM is partnering with Visa for offering Visa’s tokenization services to its IoT clients. Every IoT device or thing can be made a point of sales (PoS) terminal enabling transactions, such as a car ordering spare parts and a refrigerator ordering groceries.

Here are some potential use cases for banking of things in consumer finance and banking operations, each designed to simplify or improve some aspect of banking:

► Biometrics can be introduced for customer authentication at branches and ATMs. So, customers would no longer have to carry documents or cards to identify themselves during banking

through physical channel. Advanced video analytics (smart sensors embedded within ATMs and CCTVs) can help banks to address the problem of customer validation during ATM transactions. In general practice, banks authenticate customers at ATMs by payment card.

However, there is no way to ascertain if the person swiping the card is the actual card owner. Sensors in the ATMs and CCTVs can alert the system about any  inconsistencies and security measures would either prevent or delay dispensing cash unless the identity of the person is established.

inconsistencies and security measures would either prevent or delay dispensing cash unless the identity of the person is established.

► Now-a-days many healthcare companies and hospitals are providing personalized medical consultancy for blood pressure, sugar levels to cardiac health to patient through collecting data from wearables implanted sensor tracking system. Bank could partner with healthcare companies and hospitals and can play a consultative role regarding personalized health tips, discounted membership offers and financial supports as well. New products can be designed from the bank’s side to offer custom

payment options based on subscription or pay per use models.

► Another use case could be that of tracking usage of assets such as automobiles, provided to customers through auto loans. Data captured through sensor devices can be analyzed and behavior

patterns can be determined to offer products and services at different pricing.

► Data security is a major apprehension. Data privacy and security measures need to be unquestionably taut and effectively instigated. As custodians of customers’ money, banks have to focus on providing useful and secure innovations while protecting customers’ privacy and adhering to exacting compliance measures.

► Data security is a major apprehension. Data privacy and security measures need to be unquestionably taut and effectively instigated. As custodians of customers’ money, banks have to focus on providing useful and secure innovations while protecting customers’ privacy and adhering to exacting compliance measures.

► There are many low cost wearable devices available in the market and banks can extend a very important requirement like updating real-time customer balances to

their watch. It will help customers to keep track of their debits and credits and view balances on their watch, without navigating the bank’s web portals or apps

► The geo-location data can be fetched from the user’s mobile that can be used in real time for fraud prevention.The user’s device location data can be matched with the transaction location at the POS (point of sale). If it matches, the transaction can be approved – all in a matter of milliseconds.

► The geo-location data can be fetched from the user’s mobile that can be used in real time for fraud prevention.The user’s device location data can be matched with the transaction location at the POS (point of sale). If it matches, the transaction can be approved – all in a matter of milliseconds.

► Personal mobile wallet allows fund transfer via a mobile number. You can also request for funds from others, request for payment links, pay your bills, and donate money to charitable organizations and more (Like DBS PayLah). You don’t need to know the account number and name for money transfer instead you can send transfer request through SMS authorizing the mobile number of the payee, which is tagged with the bank account number.

Legacy IT Infrastructure is one of the major challenges. The lack of customer centric approach and limitation on internal process and people up-gradation initiatives (in terms of digital transformation) prevents the breakthrough of banking sector performance.

Possibilities of IoT is endless. The platform is already there and we need proper plan and utilization of the platform. The whole landscape of financial services is changing. We also need to change our mindset in terms of delivery and integration. New ventures, channels and products need to be introduced to make the things happen.

At present, we are at technical disruption phase globally. Partnering with start-ups, third party appsservices is desired and feasible to enhance quick progress in financial industry for digital offerings. Connected digital ecosystem is the way to handle the digital disruption, and financial services can serve as the backbone for upstream and downstream value chain.We can’t avoid the changes in banking industry. To keep up with that, we need vision for technology adoption to sustain in the market as well as for being a part of tomorrow’s market leaders.

{kind=link}