Khandakar Kayes Hasan joined LankaBangla Investments Limited as Deputy Chief Executive Officer in September 2014. Prior to his current position he worked in various positions in leading foreign Commercial banks for over 13 years. He started his career in Corporate Finance Department of LankaBangla Finance Limited back in 1999. He also worked as the manager of Leasing Department of LankaBangla Finance Limited from March 2000 to July 2001.

After that he joined Standard Chartered Bank in Wholesale Banking department as Credit Control Manager from July 2001 to March 2005. He continued his service in SCB as Business Planning Manager of Origination & Client Coverage department from April 2005 to June 2010. He also held the position of Senior Relationship Manager of Origination & Client Coverage department for the period of July 2010 to October 2011. Later on he joined another foreign commercial bank HSBC Vice President of Risk Analysis Unit in 2011.

He completed his graduation and Masters from Physics Department, University of Dhaka and completed his MBA from Institute of Business Administration (IBA), University of Dhaka with major in Finance. Being passionate about achieving excellence in Financial System and Financial instruments he obtained prestigious CFA Charter from CFA Institute Charlottesvile, VA, USA in the year 2007. He is also a renowned chess player and won many local & national awards in various chess competitions.

LankaBangla Investments Limited (LBIL) is a fully owned subsidiary of LankaBangla Finance Limited, one of the leading Non-Banking Financial Institutions in Bangladesh. LBIL is engaged in providing investment banking services and investment management services for its clients. We sat down with the CEO of LankaBangla Investments Khandakar Kayes Hasan, CFA at his office in Motijheel, during which he talked in detail about fund management, LankaBangla’s vision, the future of investment banking in Bangladesh, the current state of the capital market and many more related topics. Mr Hasan’s understanding of his field is impressive and his passion is inspiring. All of that have been captured in this interview, printed here in full:

Fintech: We know that you have over a decade of experience in commercial and investment banking. How did you get started in this career?

KKH: I studied Physics at Dhaka University, where I did honours and masters in Physics. After that I did MBA from IBA. In March of 1999 I joined Vanik in the corporate finance department. I was in corporate leasing for about two years and four months. In July 2001 I joined Standard Chartered. I was in credit and corporate banking there for about 11 years. So, actually quite a bit of my career is in banking. After that I was in HSBC for almost three years. Originally, my field was not in the capital market. I pursued CFA when I was in Standard Chartered. Although this is not really relevant to commercial banking, but still, it was new then. Arif bhai (IDLC) and others had already been working as CFOs then. Arif bhai’s field is actually leasing.

Fintech: Tell us about that’s how you got started in investment banking and also what is the situation in Bangladesh?

Fintech: Tell us about that’s how you got started in investment banking and also what is the situation in Bangladesh?

KKH: From my colleagues, there was Mesbah bhai from Standard Chartered, he was doing CFA then. That got me interested in CFA. I completed CFA in 2007. This pushed me into this direction.

Investment banking actually has its own charm. Although Bangladesh is in a nascent stage in investment banking. We don’t really have discretionary fund management. The deal making – merger, acquisition – we don’t have as much, like China and India.

Recently we visited India. We visited the Bombay Stock Exchange, National Stock Exchange, India’s merchant bank association AIBI (Association of Investment Bankers of India) and so on. What we saw was that there have been 50 or 60 IPOs in India just this year. They have a separate SME board, which has very flexible criterion.

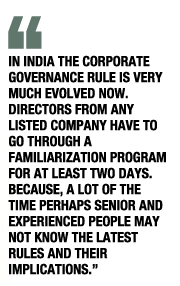

In India the corporate governance rule is very much evolved now. Directors from any listed company have to go through a familiarization program for at least two days. Because, a lot of the time perhaps senior and experienced people may not know the latest rules and their implications. Rules change a lot. So, without knowing these changes the board loses a lot of time in taking effective decisions. That’s why they do the familiarization program. That’s why they started these certification programs. It’s compulsory in derivative trading as well as in institutional fund management. When you manage clients’ fund, you have to know about the market. These things have already been incorporated in India. Bangladesh will be there too, no doubt.

Fintech: If you compare the market in India with more matured places, like if we think on the Goldman Sachs scale, where does it stand?

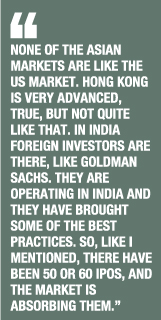

KKH: The Indian market is certainly not like the US market; none of the Asian markets are like the US market. Hong Kong is very advanced, true, but not quite like that. In India foreign investors are there, like Goldman Sachs. They are operating in India and they have brought some of the best practices. So, like I mentioned, there have been 50 or 60 IPOs, and the market is absorbing them.

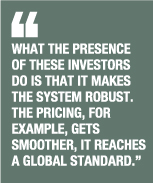

They don’t really want to work with small IPOs, they want like 80 or 100 million dollars IPOs. These things are happening and the investment by the qualified investors – they say ‘qualified investors’, what we call ‘eligible investors, – are part of foreign investment. What the presence of these investors do is that it makes the system robust. The pricing, for example, gets smoother, it reaches a global standard. Similarly, in merger acquisition, a lot is happening, like you know how TATA acquired Jaguar Land Rover. All the investment bankers are global.

So, the global banks incorporated the best practices, and then the local adopted, like we visited Kotak Mahindra Bank; they are slowly incorporating these and imposing those standards. And you have to, because you have to compete. Also from a global perspective, Indian economy is the fifth largest in the world. But still, from an economic perspective there are lots of differences with the US. Even there are many differences between India and China. But still, the progress in the financial market is being very fast in the Indian market.

Also, globally the ethnic Indian community is very advanced. At Google for example, as you know, or at Pepsi and so on. They are quite advanced in IT. They are not quite as advanced in investment banking comparatively, but still Indians are at the top most positions in many places, as you know, for example, like Vikram Pandit of Citigroup. They are ahead and these things are helping them.

Fintech: Going back to your work, you joined here in 2014. Talk about your role as the CEO and your experience

KKH: Pre-2011 merchant banks mostly were limited to being an offshoot of overall finance. LankaBangla Investment was also a part of the financial division. It was called merchant banking division. Also the operation was independent.

Anyway, at that time the merchant banking was occupied with basically one thing, which is margin loan. The market was taking shape and getting started then. Merchant banks got their main income from margin loans. Some was from their portfolio management. Some merchant banks always did issue management.

After that, at around 2010/11, what happened was trigger sell of margin loans. Because when the market falls, if you don’t trigger sell then equity gets depleted very quickly. Regulator supervision wasn’t very strong then. So, merchant banks suffered severely.

After 2011 we focused more sharply on issue management. At this moment the LankaBangla issue management team is a big team. In the last 4 to 5 years we have done 12 issue work. So, after the focus on issue management our diversity enriched and through this LankaBangla Investment got a branding.

When we started working for United Power, the book building process had been closed since 2011. We brought United Power in 2014. In 2015 we worked complying with the revised book building process. After the revised rule in December 2015, we also were the first to work under it, we did Aamra Networks’ work. From August 6 Aamra will have public subscription. 60 percent subscription for the eligible investors have been completed, now the rest 40 percent public subscription is set to be completed.

When you try to establish something you have to go through certain challenges. When the approval for bidding came through for United Power, the market was below four thousand, you may recall when the market was at 3600/3700. We had to complete the bidding of United Power. It was a mammoth task. Book building had been on a pause for four or five years. People did not have trust on the market. But we managed to stay in the market at Tk72. Later on the price of share went up. After dividend and other costs, they are still trading at about Tk180. In case of Amra, as well, there were many challenges after having complied with the new rule, acclimatizing and bringing into the market. When you do that there are changes in prospectus, there are new things in the regulation and there is a learning curve for us as well. Particularly in book building, when you have a new bidding software you have to have that checked with DSE to see if there are any violations of any rules. Because any violation will remain as a reference.

But after we did all that, LankaBangla achieved a branding value for issue management in the market. Our team is working hard and a rapport has developed with the regulators.

Fintech: what was your role during this process?

KKH: I took charge in 2014. But the issue management team had been working since 2011. What I have done is, although the market for that has not developed yet, but along with issue management we started an investment banking service team. This is mainly concerned with commercial paper, bonds, merger acquisition, demerger and so on. Although the market is quite small, we have done a number of deals. So, when the market will develop we will be ready for that. There aren’t many IPO work at this moment, for example. We aren’t doing more than 2 or 3 per year at this moment. But we want to be prepared, so that when there is demand we can do 20 or 30.

Fintech: But how certain you feel about this growth?

KKH: Well, let’s say it doesn’t grow that much. But even if it’s not 20-30, it’s certainly possible to do seven or eight for an issue manager. So, we want to have our resources ready for that. You can’t build an investment banker overnight. They have to be familiar with accounting, taxation rules, laws. They are now building strength, so that we can capture the market when the time is right.

Fintech: What are the regulatory challenges you face?

KKH: In our field we need certain regulations actually. India has progressed a lot in this regard. They have Companies Act 2013, whereas, we still have the old Companies Act. All mergers and acquisitions are conducted under two clauses, 228 and 229. BACC is also developing merger and acquisition rules. So, these changes are on the horizon.

On the other hand, public issue rules cover IPO and debt. But for debt, in bond specifically, the public issue should be different. In bond market we are not seeing public issue. We have only two publicly listed bonds, which are Islami Bank bond and the zero coupon bond of BRAC Bank.

In India there are separate sets of rules for public issue of bond. We need something similar for debt public issue. I think that is a regulation change we need. For IPO, we should move toward more of a disclosure based regime in practice. In India an IPO can be listed within four to five months, counting from the time of application. It’s a big thing in India; how quickly the process is completed is very seriously taken. You get a sense of how seriously this is taken when you hear the Indian Prime Minister Narendra Modi refer to these in his speeches. He often mentions these matters, (says things like) “we have shrunk down the processing time from 12 days to 5 days; it used to go through seven desks, now it goes through two desks,” etc. This really assures the foreigners that there is increasingly less bureaucracy and more transparency. This really helps the market. So, you see the reflection of that, Sensex in Indian stock market crossed 33 thousand points. That gave great financial boost.

So, on the regulatory side we need to shorten the time of approval and speed up the due diligence. There has been draft amendment for public issue rules recently. From a rules perspective book building is disclosure based. There (in India) SEBI doesn’t give any approvals for IPO. What it does is that it gives approval in principle, but not related to pricing. If we can follow the time based model here, then we can do the issues quicker.

Ultimately, there are two main objectives for a company going public; one is the fund requirement and the other is to have a branding as a public listed company as well as having an exit option. For the fund requirement part, we always say that long term finance should be always based on equity. If you don’t have equity, then naturally you form equity with others. You raise equity and then you go to a project expansion. But if you need one or one and half year for one project after you decide to come to equity, then no business will actually be stagnant for that time period. They have to arrange the project. Then there is the matter of when the fund actually comes through and so on.

In India they do QIP or Qualified Institutional Placement if a company needs fund within a month. So, for example, when there is a bidding on a public platform it can be done within two days. Say, a big company needs to raise fund, maybe Reliance needs two thousand crore rupee, it can be completed within a month including getting approval and other prerequisites. There is that option. If an IPO gets done in five to six months, then that is reasonable.

Fintech: So, without the proper legislative instrument the regulation can’t move forward.

KKH: I talked about the Companies Act, but this is not BACC’s domain. It’s purely legislative. It’s not that BACC is against these changes. But it’s not really within their scope. Like the FRC (Financial Reporting Council) was facilitated largely by BACC.

There is an apprehension about adverse reporting in the media. Maybe our regulators feel a little shaky about this. We have to move from a control regime to disclosure regime. One of the problem with the control regime is that market doesn’t achieve maturity. India has crosses that phase. It is a challenge for us.

Fintech: We have been covering the national budget and the discussions around it. Do you have any thoughts that you want to share?

KKH: I am not an expert in this, but I think our budgets are kind of turning into focused on one-year type. So, now there is an election ahead, therefore, maybe the budget has been devised as election centric. The VAT rule may need modification but it needs to be there. In India GST is similar. Modi’s demonitisation caused suffering. But overall, the economy accepted it. But I would say though, that our budgets have been successful in moving the economy forward to some extent. That is a success, but there needs to be long term vision.

Fintech: You have implemented IFS 9. Is that across the board in your companies?

KKH: It will be across the board but LankaBangla Finance started it. There are separate IT divisions for Finance, Security and us. But it will be uniform with certain exceptions.

Fintech: Tell us about how you are utilizing and adopting automated platforms, Cloud etc.

KKH: Retail investors will ultimately move to mobile platform. Clients are increasingly doing mobile trading. Some of the things are not yet available in the Bangladeshi market, like the machine based algo-trading. Globally two third of the trading are machine based. From that aspect fintech is very important. Generally, the financial industry stays a little behind in technology, compared other industries. Because of the security the move toward absorbing the disruption is slow. Capital market is more technology driven than the money market.

Fintech: We interviewed the DSE MD last month and he was talking about how their app employs state of the art models, uses the NASDAQ algorithm, but because of restrictions on online trading that ultimately doesn’t count in trading. But they are focusing now more on capitalizing the data.

KKH: Yes, it is very data centric now. As the DSE is a data source in the capital market. DSE is thinking about how to package that data and sell.

Fintech: To what extent commercial banks occupy the same space in terms of competition with investment banking?

KKH: As an investor commercial banks are a big stake holder in the capital market. When we talk about who invested how much fund in the capital market, 90/95 percent of the capital are from the commercial bank lending.

So far, the debt issuance is mainly through the commercial banks. There are some private issuance, but that is less than five percent. Since they are regulated by the Bangladesh Bank they can’t always get the exposure to the capital market. When commercial banking does a presence share or invest in non-listed preference debt, that is considered as exposure to the capital market. They can do 25 percent in capital. But actually capital market exposure should be of a listed company. Because only listed companies have the secondary market risk.

As a competition commercial banks are not competitors of merchant banks in terms of debt share, in raising capital in the overall market. Increasingly merchant banks are getting the capabilities in other segments, like zero coupon bonds, which was previously the domain of commercial banks. I think investment banks are getting momentum. Commercial banks have challenges, as do investment banks, but they have problems of bad loan and so on. In corporate and institutional banking merchant banks are slowly growing. It will be difficult to reach the stage where India is at.

Fintech: Which segment(s) you are focusing on now? And tell us about your projection about those segments.

KKH: Our strength is in IPO, IPO rights, merger and acquisition. Also we have done a number of debt issuance and now we have a good database. On the area of portfolio management our focus is actually on discretionary portfolio management. We have a product called LankaBangla Nishchinto, which provides a monthly DPS. Another one was AlphaPlus, where we manage the fund. Other merchant banks are doing this as well. Globally many different schemes are practiced like pension fund and discretionary funds like that. But formal fund management practice is not very prevalent here as of yet. But still we are focusing on this. Discretionary fund management is where the growth will be in Bangladesh.

Retail investors often have the hoard mentality. A large or a mature investor buy a share and reach a price. When they collected the share it may have had a buying price. Then the share is sold and the retail investors are seeing it later, when the price had been altered and spiked quite a lot. That makes them counter to the large investors. Reasons like this makes expert fund manager necessary. So, we are really focusing in this area.

Fintech: What do you think about our magazine and what kind of role it can play in contributing to market education?

KKH: Financial education is needed at all levels. From novice investors to the regulators to company chairmen and directors, everyone needs the education. That’s why I think your magazine is for all of these groups. So, I think you should think about all of these different segments and in addition to advanced materials you should also have accessible articles that people can read and understand. That is very important.

I think your coverage from many different sectors is really good. Your interview with Arif bhai, Mamun Rashid bhai is something from which I can learn. There’s always something that I can learn from these people. The PwC post budget session that you covered, will not probably be something important for a layman investor. But many economists may use this as reference. A fund manager can learn from this too.

Fintech: Thanks very much for your time.

K K Hasan: You are welcome. ■

{kind=link}