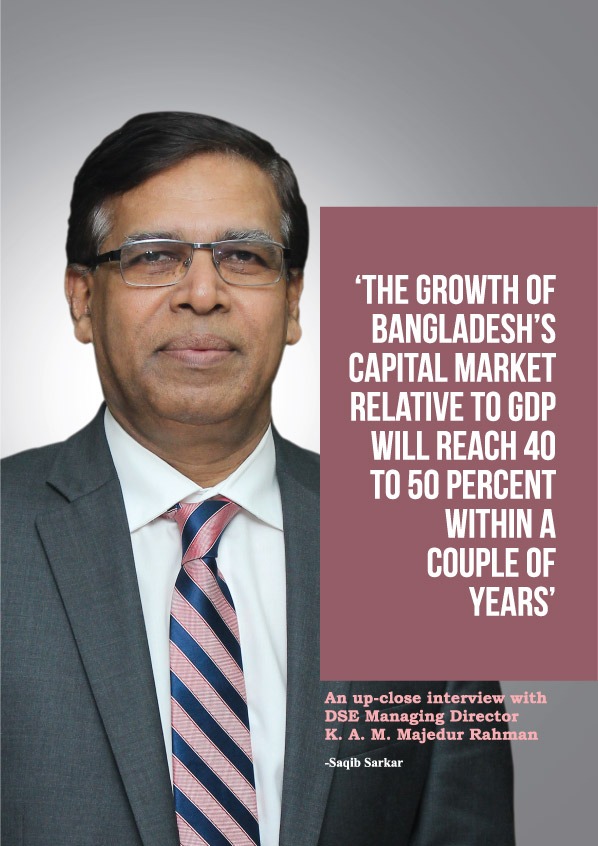

K. A. M. Majedur Rahman joined as the Managing Director of Dhaka Stock Exchange on July 12, 2016. Mr. Rahman, a former banker with expertise in strategic planning, business development, information technology, risk management and capital market operation has worked in key positions in banks of Bangladesh, Australia and the Middle East and Africa. Prior to joining at DSE he was working as a consultant at USA based E-Currency Mint Incorporation and Senior Advisor South Asia, Aspen Capital Solutions USA. He concluded his banking career as Managing Director and Chief Executive Officer of Premier Bank Ltd. Majedur Rahman started his career with Grindlays Bank Limited in 1981 as a Management Trainee. During the long span of his banking career, he held key positions in Retail, SME, Commercial, Investment Banking, Trade Finance, Internal Audit and Operations management. Majedur Rahman worked overseas over 10 years and returned home in 1997 to lead Standard Chartered Bank’s consumer banking business introducing the first ever ATM network and online banking in Bangladesh. He pioneered the introduction of asset backed Zero Coupon Bonds in Bangladesh. He served as the CEO and Managing Director of the Premier Bank Limited until February 2015. Earlier, he had set up the operations of Bank Alfalah Limited in Bangladesh as the first Country Head. He had served as Additional Managing Director of AB Bank Limited, Deputy Managing Director IPDC Bangladesh Limited, Senior Executive Vice President of Dhaka Bank Limited. Other key roles he performed include Group Internal Auditor of the London based Grindlays Bank, Senior Business Analyst at ANZ Bank, Melbourne and Manager Business Process. Re-Engineering of ANZ Bank in the Gulf region. He has also worked as the Assistant Vice President of Dubai based Mashrek Bank. Majedur Rahman attended premier institutions Faujdarhat Cadet College and Dhaka University for schooling, undergraduate and postgraduate education. He has attended Senior Management Development programmes at Said Business School, Oxford; London Business School and FMO Netherlands. Mr. Rahman has also attended special training on Risk Management at the prestigious Institute of Risk Management, United Kingdom.

Sitting behind the large executive desk in his rather small office at Toyenbee Road, K. A. M. Majedur Rahman looks and sounds more like a Liberal Arts professor than a man who deals with the complicated trends and probabilities of the stock market. Indeed, reading politics and history remains Mr Rahman’s leisure activity and passion from his student life when he had aspired to be a career diplomat. A lifelong banker who worked in the most responsible positions within the country and internationally, K. A. M. Majedur Rahman became the managing director of Dhaka Stock Exchange (DSE) exactly a year ago. With over three decades of experience in the financial and banking sector he has a wealth of industry knowledge to share. Fintech spoke to Mr Rahman to learn about his extraordinary career and know about his thoughts on subjects related to the banking sector, stock market and fintech. Here is the full interview for our readers.

FINTECH: You started your career at Grindlays Bank in 1981. You have over 35 years of experience in the industry. Could you talk about your journey thus far?

KAMMR: It’s a long story. Basically, I never really thought, even in my wildest dream, that I would be a banker. The perspective in 1981 was that it was generally a tough time for Bangladeshi people in terms of financial solvency. I lost my father early and that’s why my goal was to become established in the professional life as soon as I can. I worked a lot during my student life, like journalism and a little bit of radio and television work as well. I used to write articles in Bichitra in those days. I got into the banking industry by accident. There was an trends and probabilities of the stock market. Indeed, reading politics and history remains Mr Rahman’s leisure activity and passion from his student life when he had aspired to be a career diplomat.

A lifelong banker who worked in the advertisement in a newspaper for a job, which I applied for and got selected. And then we had a probation period for a long time after I joined Grindlays Bank as a management trainee. I and three others joined at that time in that position. They were Mamun Sattar, Anwar Shahid and Wahid bin Dewan.

After we completed the management trainee period I was posted to Chittagong and put in charge of a branch. At that time, I thought I was in that job for a short time. I wanted to complete my masters and then enter civil service. I wanted to be a career diplomat. But I soon found out that the banking world is really fascinating and I was doing quite well too. So, I decided to continue in this sector.

After that I was the first officer from Grindlays Bangladesh to be posted overseas. I was posted in London as a group internal auditor. It was in 1985. From there I went onto work in many places across the globe including places in Africa and Middle East, in Pakistan and Jordan. I came back to Bangladesh in 1987. At that time Grindlays was having difficulties with a branch in Mirpur. I was made the in charge for that branch. I started putting in serious efforts and that eventually made that branch the most profitable after the Dhaka’s main branch. As a reward I was transferred to Chittagong, again. Chittagong was very important to the bank at that time, because all the import and export trades were there. I was made the ‘Area Operations Manager’ in Chittagong. I was there for a couple of years.

After that I was the first officer from Grindlays Bangladesh to be posted overseas. I was posted in London as a group internal auditor. It was in 1985. From there I went onto work in many places across the globe including places in Africa and Middle East, in Pakistan and Jordan. I came back to Bangladesh in 1987. At that time Grindlays was having difficulties with a branch in Mirpur. I was made the in charge for that branch. I started putting in serious efforts and that eventually made that branch the most profitable after the Dhaka’s main branch. As a reward I was transferred to Chittagong, again. Chittagong was very important to the bank at that time, because all the import and export trades were there. I was made the ‘Area Operations Manager’ in Chittagong. I was there for a couple of years.

After that I went abroad once again. This time I went to Mashreq Bank in Dubai. But it was called Bank of Oman then. I had a role in the bank’s transformation process, starting from automation, a new product line, new business and all other related things. The work I was involved in there was quite important. From there I once again came back to Grindlays Bank in Dubai. The General Manager in Dubai knew me very well; so, he asked me to join to carry out a few challenging work they had at that time. From there I was transferred to Australia. At that time ANZ Grindlays Bank was bringing in resource persons from different countries to develop the entire commercial banking system.

So, I was there doing that work when I suddenly felt that I should return to Bangladesh. I came back in the middle of 1997 and joined Standard Chartered Bank as the head of retail banking. It was called consumer banking then. The consumer banking wasn’t very developed at all back then. What they had at Grindlays was called personal banking. So, at the Standard Chartered we put our main focus on automation, as I had been working on automation before. My intention was to do something that will bring about a positive technological change in the country. The first thing we did was to build off-site ATMs. We did the first off-site ATM in Bangladesh. It was located in front of the Shahid Jahangir Gate. After that we started to build some in Chittagong.

FINTECH: What were the technological challenges then building those ATM machines in the 90s and how difficult were those challenges compared to the current time?

KAMMR: They were enormously different and considerably more difficult. For example, we used the telephone line for ATM connectivity. Some of those dial-up lines were analogue; for instance, from our Alico Building to Gulistan we had an analogue line. From there to Mogbazar the line was digital. From Mogbazar to Agrabad in Chittagong was again digital, but from Agrabad to Andarkilla was analog. And finally from Andarkilla to where we were building the ATM at the GSE intersection, the line was analog.

It was frustratingly difficult to find a pair of good telephone connection points. We couldn’t have light and electricity (at the booths) even. All of it was challenging.

FINTECH: What kinds of business challenges you had and how did you go about solving those?

KAMMR: There were many business challenges. We introduced personal loans as a new product in retail banking. We also started another product called the Money Builder. Other banks started the same products after we did it. We also started something else that was new. We started direct sales. There was no concept of direct sales in Bangladesh.

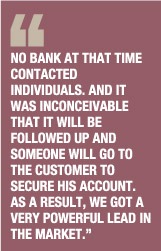

We had marketing relationship officers, but they were called PFC or personal financial consultant then. We had four of the PFC for phone banking. We introduced phone banking too, by the way. Anyway, we didn’t have much traffic in phone banking. The incoming traffic was light enough to be handled by two persons. The manager for that team was Rahnuman Ahmed. I asked her to do something new. I told her that she will be given a database and she will make outbound calls. I asked her to try that and see if that works out better. And it did. Eventually, we got excellent results from that. No bank at that time contacted individuals. And it was inconceivable that it will be followed up and someone will go to the customer to secure his account. As a result, we got a very powerful lead in the market. Grindlays was the biggest bank then. The Standard Chartered was quite small; we only had three branches. We gave them a run for their money with just those three branches. At one point, of course, Standard Chartered Bank acquired Grindlays, as you know.

The acquisition period is normally quite tumultuous, in the sense that the business focus gets lost somewhat. I decided to work at local banks and joined Dhaka Bank in 2002. When I joined, Dhaka Bank was in a very traditional set up. So, we decided that we will do branding for the bank and implement a Core Banking System. We started Core Banking System at Dhaka Bank and it was one the first here. All of this helped build a great image for Dhaka Bank. At that time local banks did not have access to ATM networks. We built a new network called ‘e-cash’. After that the Core Banking System was set up in all the branches and after all branches were connected and we started internet banking.

In 2004 I left Dhaka Bank and joined IPDC. One of the reasons for joining was that it was in the process of starting up a bank. IPDC was mostly foreign owned at that time. The government had 25 percent share and the rest was owned by the Common Wealth Development Corporation, IFC and the Aga Khan Foundation. It was like a development financial institution.

They wanted to put a bank together from the other banks owned by the Aga Khan Foundation. The work for that was going on. But it got delayed and during that time I was offered to join Bank Alfalah. Bank Alfalah had just bought Shamil Bank and they were about to start operation. So, I was asked to come in as the Country Director and I joined. I was there until 2009, after which I joined AB Bank. I had similar challenges there with product development, business development, and technological development.

After AB Bank I joined The Premier Bank. It already had the effective set up, mostly. But, unfortunately, the business growth there was inadequate. Also there were problems with the implementation of the technologies they had.

FINTECH: You are not from a technological background academically. How do you approach technology and what is your view of using technology the right way?

KAMMR: That’s true. My formal study was in International Relations. But somehow I find using technology very interesting, no matter where the technology is being applied. For example, I use an app from Oral B for brushing my teeth. The app directs you to brush the places you missed. So, technology interests me in all its forms. I’m very comfortable in using technology as well. There isn’t much difference between the way I use my computer and my iPhone.

Just a few days ago I was looking for a book when I was in India. I couldn’t find the book but found a Kindle Reader. I bought the Kindle Reader for four and a half thousand rupees and now I have 25 lac books. That’s what technology has made possible.

FINTECH: Do you read a lot? What do you read normally?

KAMMR: I love to read. I actually don’t read about technology a lot. One of my interests still remain politics and history. So, I read a lot of ‘international relations’ and history books. But that  discussion will lead us out of our subject today.

discussion will lead us out of our subject today.

FINTECH: It would be very interesting though to know more about what you read. But to go back to where we left off, you talked about your career in the banking industry. Please tell us what you did after AB Bank and how you came to join the DSE.

KAMMR: Yes, of course. Coming to the DSE is a whole other story. After I completed my work at AB Bank I got into a Silicon Valley company. You can call it a fintech company. The company is called eCurrency. It’s not like bitcoin, but it’s basically based on encrypted numbers, which can replace paper (money). A lot of work is going on in this field and it has already been recognised in Africa. It was supposed to be introduced in Bangladesh too, but unfortunately the Bangladesh Bank incident put that on hold. So, I got the chance to get into the capital market as I was working there.

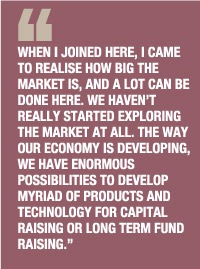

I didn’t have any expert knowledge about capital market. I never really had much interest either. When I joined here, I came to realise how big the market is, and a lot can be done here. We haven’t really started exploring the market at all. The way our economy is developing, we have enormous possibilities to develop myriad of products and technology for capital raising or long term fund raising. So, that’s where I want to concentrate and I have started doing a lot of that already. I think there is scope for everyone to contribute toward the development of this market.

FINTECH: You have studied risk management in UK. Tell us about its applicability in Bangladesh.

KAMMR: Actually, it is quite a new area in Bangladesh. There is operation risk, business risk, administration risk, market risk and so on. These all come under the ambit of risk management. So, when work on risk management first started, I was lucky to have worked as the Chief Risk Officer at AB Bank. It was an extra role for me as the Additional Managing Director. I then realised that this is a very specialised area of work and you need a set of qualifications to do it properly. I then contacted the Institute of Risk Management in the UK and went there to do a course. Other than that there is a British organisation that have professional risk management programs for the financial sector. I also contacted them and still keep in touch with them. If you have a membership with them and do the qualification course, then you can attend many sessions by them throughout the year. These are delivered through Webex. So, they have sessions on cyber security, fintech, blockchain and so on. And it’s very accessible; I can just pop in my headphones while I’m in the car and participate in the seminar.

FINTECH: Last year you said in a press conference that DSE should monetize its huge data bank and make it a source of revenue. What happened to that?

FINTECH: Last year you said in a press conference that DSE should monetize its huge data bank and make it a source of revenue. What happened to that?

KAMMR: Yes. So, what happens is that in capital markets one of the income stream is selling data. But we don’t have that practice in our country. What we have is that everyone copies data and exchanges that freely. Some even capitalize on it and sell the data. But what we want now is to build an authorized data selling process. So, in the process we have already entered into an agreement with Bloomberg, we are going to get into an agreement with Reuters and many other organisations. We will be able to earn a good revenue against this. We are hoping to get a substantial amount from Bloomberg. In other countries, data selling generates at least ten percent of the trading income.

FINTECH: Compared to a highly specialized stock exchange like NASDAQ where do you see DSE is?

KAMMR: Actually if you look at the whole ecosystem then you will see that we have a lot of potential. In case of NASDAQ or New York Stock Exchange, these are considered main places of financing for capital raising. But in our country we are asking the banks for long term investments. In reality banks cannot provide long term financing. Banks can do it for five years or seven years. In the past the sizes of our industries were small. So, there wasn’t a necessity for capital that much. But now those companies are much bigger. As they need more capital now, they have to come to the public. From that aspect our capital market is growing.

The growth of our capital market relative to GDP is currently only 21 percent. It should be at least 50 or 60 percent, may be more. In America it is over 100 percent. In Hong Kong it is 400 percent and in India it is 70 percent. I think we will reach 40 to 50 percent within a couple of years. For that what we must do is to add more products. We have to make it what is called the ‘Multi-Aasset Class Exchange’. Currently we have only a single product – we only raise capital and trade shares. At the same time, to make it successful we have to create investors and professionals who can handle this. We have to invest heavily on this. We don’t have that preparedness currently. We have a lot of work to do here.

FINTECH: Prime Minister’s IT Advisor Sajeeb Wazed said that he would take initiative to get foreign investors. What is the update on that?

KAMMR: After we had the demutualization, we are required under the Demutualization Act to seek out and get what is called strategic investors. A strategic investor is like a technology partner who will have technology experience or capital market experience or they can be financial institutions. We are working on this. We are hoping to reach a decisive stage by this June.

FINTECH: You wanted a tax holiday for three years as well as exemption from capital gain tax on block shares in the fiscal year 2017-18. How the government has responded to this?

FINTECH: You wanted a tax holiday for three years as well as exemption from capital gain tax on block shares in the fiscal year 2017-18. How the government has responded to this?

KAMMR: Actually the response will come with the Finance Bill. We haven’t got the response. But our proposal is that when we had the demutualization we were supposed to get a five-year tax holiday. After a year it was re-imposed and then we applied again and we were granted a second year. So, we have requested that it is extended to five years, because we have still need a lot of technological development.

FINTECH: DSE has a very modern and high standard app. Tell us about how it was developed and the security aspect.

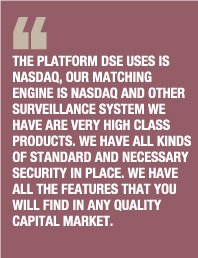

KAMMR: We employed a world class company called Flaxtrade to do this for us. The platform DSE uses is NASDAQ, our matching engine is NASDAQ and other surveillance system we have are very high class products. We have all kinds of standard and necessary security in place. We have all the features that you will find in any quality capital market. It is getting increasingly popular. But one of the issues we have is that complexity of the law. We still need paper signature for example. If we can overcome and go past these things, then we could make the most of it. And the app is not for information only, you can carry out trade through it. It is fully cyber security compliant. We maintain the highest security compliance. IT security is one of the most important areas for us. Everything is automated here.

FINTECH: What are your thoughts on new disruptive technologies like big date and how to take advantage of them?

KAMMR: Disruptive innovations are not affecting capital market as of now. But I don’t think it can’t happen or shouldn’t happen. I think we will be quite positive about it. However, the technology in the capital market is quite complicated and expensive. The way innovations are happening in other areas like retail banking or FMCG is different. For the capital market they don’t happen the same way. It will happen perhaps, but not at that speed.

FINTECH: After a long time in the banking industry you are here now. What is your personal feeling working in a different field to what you worked in for the most of your career?

KAMMR: I think if I could be in this sector from the start of my career, or at least if I had gotten into it even five years earlier I would enjoy it more. I am enjoying it very much now anyway.

FINTECH: Thank you very much for speaking to us.

KAMMR: You are welcome.

{kind=link}